Secondary Tariffs or Tighter Sanctions? Strategies to End Russia’s War in Ukraine

Earlier this month, U.S. President Donald Trump threatened secondary tariffs of 100% on any country trading with Russia if there is no deal to end the war in Ukraine within 50 days. This proposal parallels a bipartisan bill in the U.S. Senate, sponsored by Sens. Richard Blumenthal and Lindsey Graham, which would levy secondary tariffs of 500% on countries trading with Russia. Although both these efforts appear to be paused in the near term, there is a substantial chance they will gain traction if Russia fails to meet U.S. demands to end the war over the summer. In this article, we review these initiatives, discuss how unintended consequences may render the policies counterproductive and discuss their merits compared to the existing suite of economic measures—the core of which are the G-7 oil price cap and a growing wave of sanctions on the shadow fleet.

Secondary Tariffs to Discourage Trade With Russia

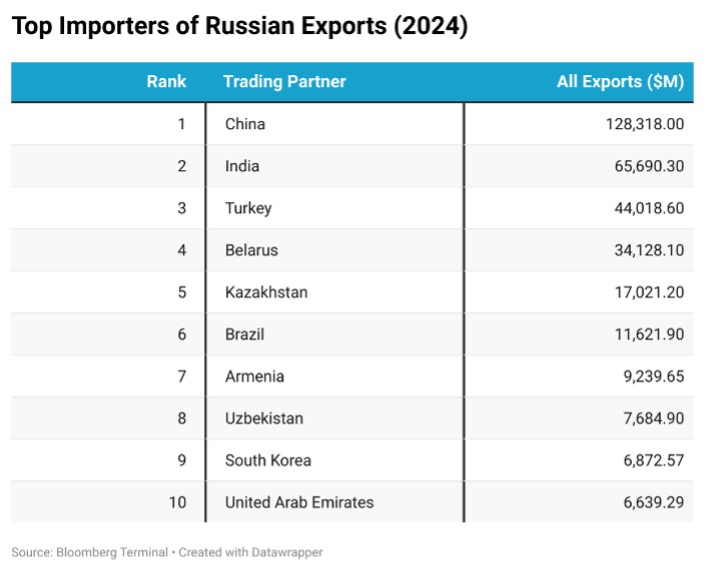

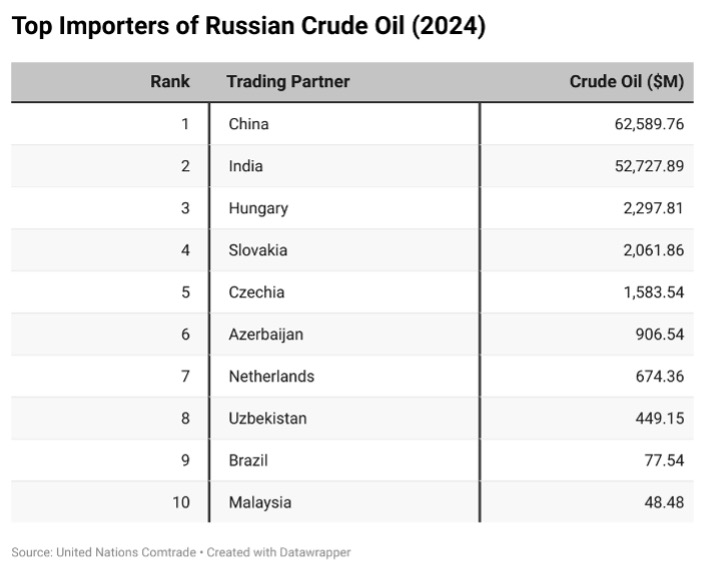

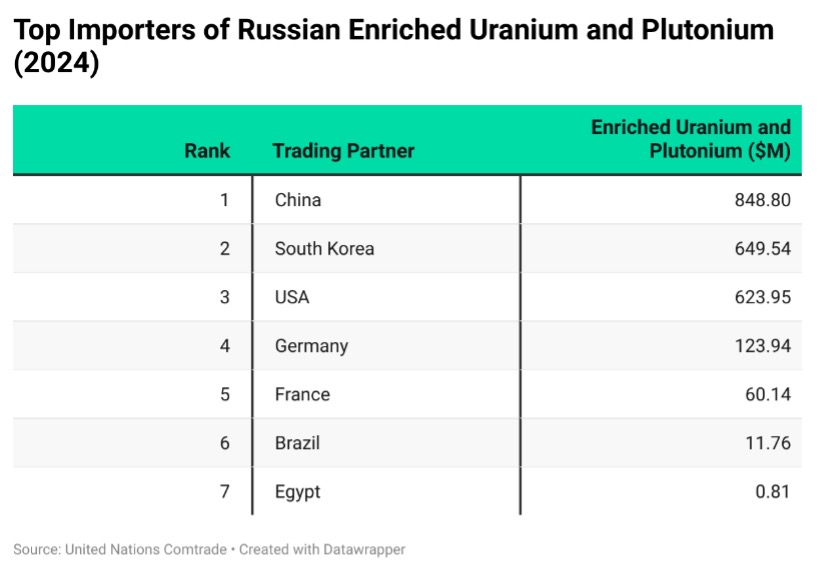

The foundation of the proposed approaches by the administration and Graham-Blumenthal bill would be to levy massive “secondary” tariffs on Russian trading partners. These tariffs would not target Russia directly, and instead would be placed on companies located in countries that import goods from Russia. While Trump has yet to specify the details of his proposal, the Graham-Blumenthal bill would assess secondary tariffs on U.S. imports from any country that purchased oil, gas, petroleum products or uranium from Russia. (See table below for major purchasers of Russian products.)

The potential response by Russian trading partners is two-fold. One option is for these nations to shun Russian exports and instead seek importers from alternative sources, thereby avoiding the steep secondary tariffs on imports to the U.S. A second option is to continue trading with Russia and therefore accept the tariffs as a consequence. The potential for widespread clandestine trading, whereby trading partners like China and India might secretly import Russian oil, is unrealistic given the massive quantities of oil involved and challenges inherent in hiding regular tanker traffic.

In the event that Russian trade partners seek to avoid secondary tariffs and identify alternative sources of imports, perhaps the most immediate economic impact would be turmoil in global oil markets given Russia’s outsized role in the energy trade. The most significant importers of Russian crude are China and India, followed at considerable distance by Turkey and the European Union (EU). In terms of refined oil products, Turkey is by far the largest exporter—followed by China, Brazil, Singapore, India and many other African and Asian nations. Should a substantial collection of Russia’s trading partners shun its exports, the immediate result will be a “shutting in” of global oil production as Russia will have limited options for selling its oil.

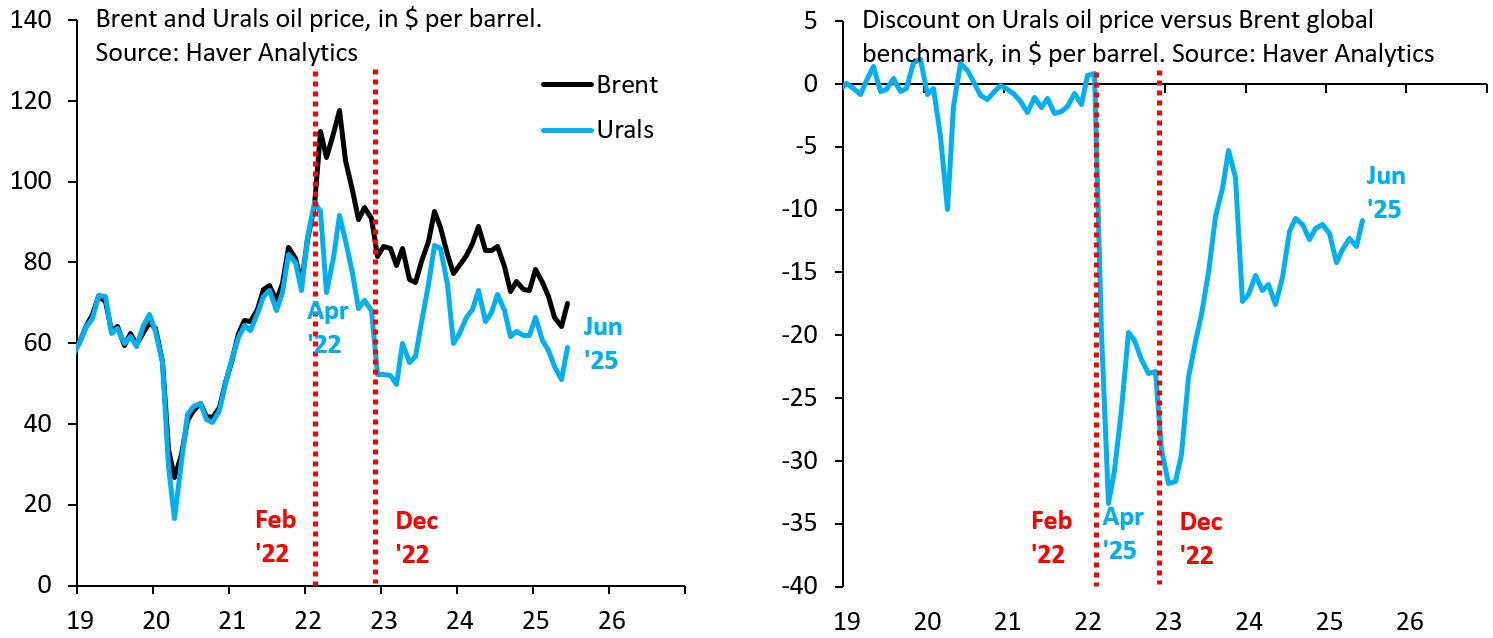

While the threat of reduced Russian exports, on its face, would be a welcome outcome, the ultimate impact could be counterproductive. An instructive example is the oil price trajectory in the immediate aftermath of the invasion of Ukraine, which provides guidance on how secondary tariffs might impact global energy markets. Shortly after the invasion, the benchmark price for Russian crude (“Urals”) fell sharply even as the global Brent benchmark rose (left chart below), widening the discount on Russian oil to unprecedented levels (right chart below). Global markets feared the West would quickly retaliate with sanctions on Russian oil exports. This possibility of Russian oil being excluded from global markets caused Brent to rise, while a “stigma” effect caused the Urals price to fall, an effect that faded only as it became clear that financial sanctions were the West’s primary tool during those early months.

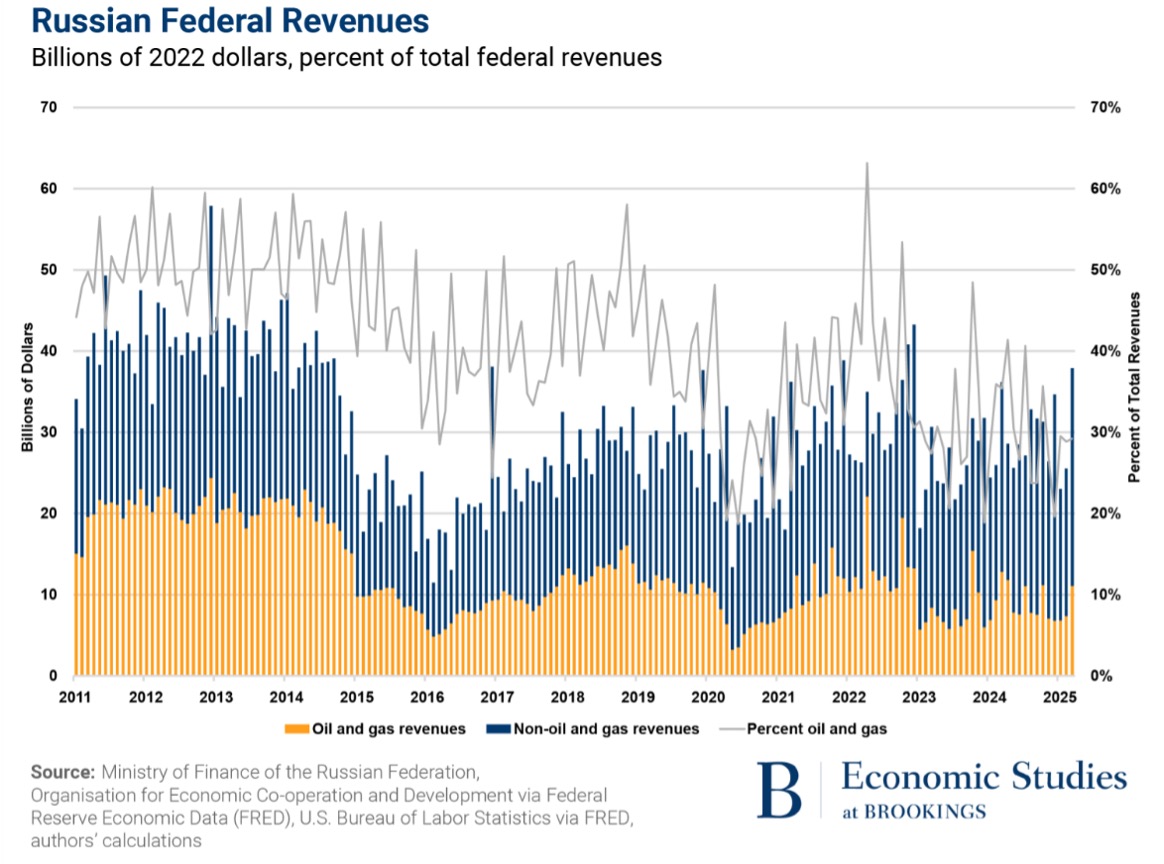

Secondary tariffs will likely have a similar effect. They will cause nations to shun Russian oil, causing the Urals oil price to fall, while projections that Russian oil will be “shut in” could spike the price of Brent. The fall in Urals would no doubt be a material shock to Russia’s war economy. As we laid out in a recent Brookings essay, tax receipts on the oil and gas sector move almost one-for-one with Urals oil price and account for almost half of total Russian federal budget revenues (see chart below). There is no doubt that secondary tariffs will materially hurt the Russian economy and fiscal outlook.

It is possible, however, that this damage to Russia comes at a punitive cost to the United States if it spikes Brent and drives an already teetering U.S. economy into recession. To illustrate, even if a portion of Russian oil is shut-in, the price impacts could be severe. Elasticities from the academic literature suggest that shutting in even 10% of Russian oil would increase the price of Brent by around $6 from its current level of around $71 per barrel; a reduction of 20% could cause the Brent price to spike by $11.1 Either of these increases would markedly raise the prospects of a recession in the U.S. and many other economies around the globe.

An alternative outcome is that Russian trading partners ignore the secondary tariff threat and choose to continue importing Russian energy. Such an outcome would immediately disrupt global trading activity and effectively lead to trade embargos to the United States. In this scenario, while energy prices would not spike, the prices of many other goods would—again elevating recession probabilities and effectively taxing U.S. consumers and destabilizing financial markets. Indeed, tariffs of this magnitude on China—a candidate target for secondary sanctions—are what spawned instability in the Treasury market in April, prompting the U.S. to de-escalate. Secondary tariffs—even if the intended target is Russia— risk re-escalating the trade war with China and weakening the U.S. economy.

An Alternative Approach: Lower Price Caps and Comprehensive Shadow Fleet Sanctions

An alternative, and in our view superior, approach is to focus on the existing set of economic measures against Russia, of which the G-7 oil price cap and sanctions on the shadow fleet are the core. This existing suite of measures has several advantages: one, as we have shown in a Brookings blog post, U.S. sanctions appear to be effective at disrupting oil tanker traffic out of Russian ports without spiking global oil prices; two, the level of the G-7 price cap and sanctions on Russian-controlled oil tankers can be scaled up and down incrementally, which gives U.S. policymakers a degree of control they would not have with 100 or 500% tariffs; and three, this year’s wave of sanctions on the shadow fleet by the U.S., EU and U.K. make this an ideal time to use sanctions even more aggressively, taking this opportunity to increase pressure on the shadow fleet through lowering the price cap and instituting further enforcement measures.

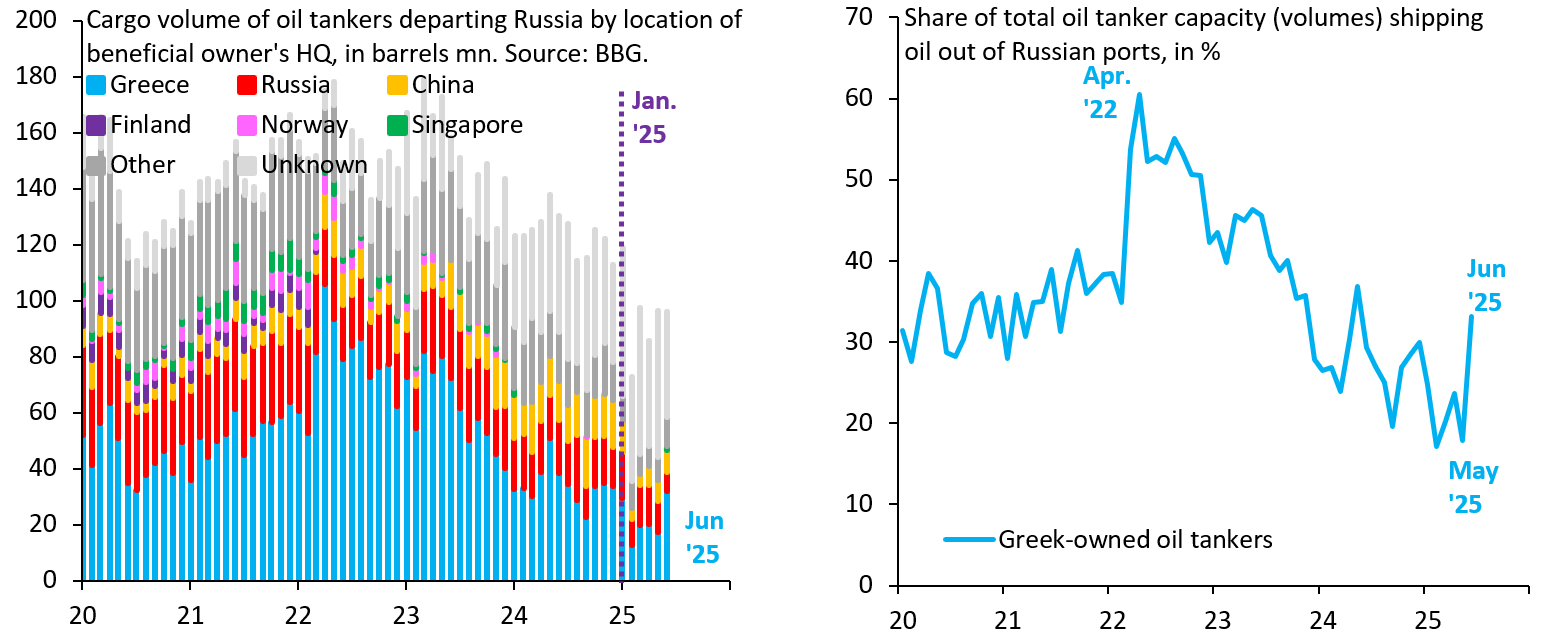

To elaborate on the first point above, as we flagged in our recent paper, U.S. sanctions on the shadow fleet appear to be effective. Specifically, it appears as though a recent wave of EU and U.K. sanctions are also having a major impact on the operations of the shadow fleet, forcing more of Russia’s seaborne oil exports back onto Western-owned oil tankers and, thus, back under the auspices of the G-7 oil price cap. The left chart above shows monthly exports of seaborne oil out of all Russian ports, distinguishing the exports by which countries own the oil tankers involved. Greek ownership has risen recently, taking the share of Greek-owned vessels back to its highest level in a year (right chart above).

This outcome helpfully aids enforcement of the G-7 cap, which relies on Western-owned vessels and associated services like P&I insurance. As a result, now is an ideal time to sanction more shadow fleet vessels, with the aspiration of achieving uniform coverage across the G-7 by sanctioning additional ships already targeted by the EU and the U.K. Moreover, the stabilization in the price of Brent oil, coupled with increased sanctions coverage of the Russian shadow fleet, presents a concurrent opportunity to lower thresholds for the G-7 caps on Russian oil prices. These provisions will deterioriate Russia’s already slumping wartime economy, but without re-escalating trade wars with U.S. trading partners or spiking global energy prices.

Indeed, the EU’s recent 18th sanctions package proceeds exactly in this direction. It lowers the price cap on Russian oil (unilaterally without U.S. participation) and sanctions an additional 105 ships, taking the total number of vessels sanctioned by the EU to an impressive 444. Additionally, the U.K. recently sanctioned 135 oil tankers and two companies facilitating the movement of Russian oil. The success of these packages will depend in large part on both enforcement, such as whether maritime countries are willing to demand sufficient insurance for Russian ships traversing their waterways, and the extent to which the G-7 can achieve uniformity across various sanctions measures. This is all the more reason for the U.S. to join forces with the EU and U.K., as opposed to going it alone with uncharted measures.

Footnotes

- Caldara, Cavallo, and Iacoviello (2019) estimated that the price elasticity of demand for crude oil is –0.14, while Helmi et al. (2024) concluded that it was approximately –0.18. With an elasticity of –0.15, and assuming that the oil market functions as described in footnote 19 of Wolfram, Johnson, and Rachel (2022), we estimate that a 1.2%v supply reduction would increase prices by 8% ((–0.012)/(–0.15) = 0.08). Note that Russia comprised 12% of global oil production in 2024.

Opinions expressed herein are solely those of the author. Photo by AP Photo, File.