Claim in 2021: Russia’s GDP per capita is 30% lower than in 2013.

Source of the claim: Financial Times (March 2021)

Writing about the Russian state’s increasing repressiveness in FT Magazine on March 14, 2021, FT’s then Moscow bureau chief, Henry Foy, mentions almost in passing that Russia’s “GDP per capita is 30 per cent lower than in 2013.” The claim—meant, together with other data, to illustrate the costliness of Moscow’s “belligerent attitude” on the world stage—surprised us since neither Russia’s total GDP nor its population has changed so drastically in the years in question. Because the author did not specify the source of his estimate, the method by which it was calculated or the year to which he was comparing Russia’s GDP of 2013, we decided to (1) pick 2020 as the last full year for which measurements of GDP were available at the time the claim was made and (2) check measurements of GDP in 2013 and 2020 in the databases of two reputable international financial institutions, the World Bank and the IMF,1 as well as Russia’s Federal State Statistics Service (Rosstat).2

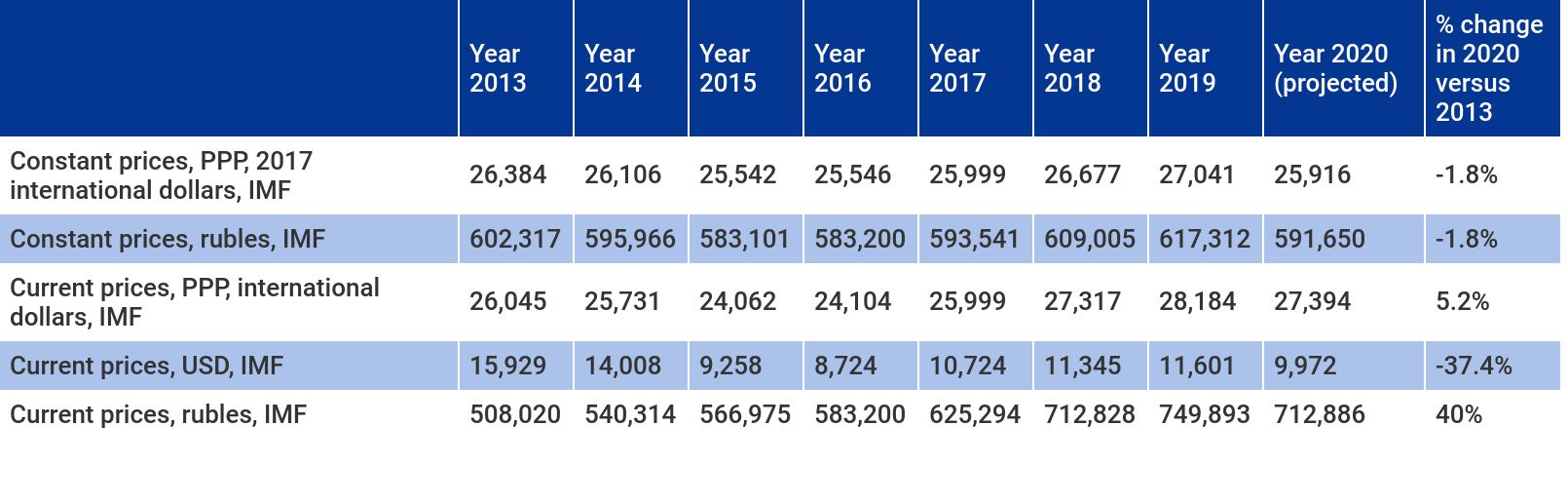

Of the IMF’s five metrics of GDP per capita, only one showed a decrease anywhere near 30% from 2013 to 2020—namely, GDP per capita in current U.S. dollars, which does not adjust either for inflation or for purchasing power and registered a decline of 37.4% (see Table 1). In contrast, two other IMF estimates of changes in GDP per capita showed a decline of merely 1.8%—calculated in inflation-adjusted rubles and in international dollars fixed at their 2017 value and adjusted for purchasing power parity (i.e., for differences in what money can buy in different economies). The remaining two metrics of GDP per capita—current prices in rubles and in international dollars adjusted for purchasing power—showed growth.

As noted by the World Bank, it is constant-price data that should be used to measure “the true growth” of a variable over time, as such data adjust for the effects of price inflation. Based on the figures below, the FT calculation of a 30% decrease in Russia’s GDP per capita seems to refer to nominal (i.e., not adjusted for inflation or purchasing power) GDP per capita and the 2013-2020 decline in this category seems driven largely by the depreciation of the ruble vis-à-vis the U.S. dollar at market exchange rates, rather than by major contractions of Russia’s economy. In short, by not providing details about the data cited, the FT’s claim may be misconstrued as an indication that Russia’s economy has shrunk by 30% since 2013—a conclusion that none of the available data support.

Table 1: IMF Estimates of Russia’s GDP per Capita as of October 2020

Source: IMF

It is worth noting that at the time the FT article was published the World Bank had data only up to 20193 but those data showed the same basic trends as the IMF data for 2013-2020. It was clear even then that the only measure by which Russia’s per capita GDP could have declined by 30% between 2013 and 2020 was current U.S. dollars, which adjust for neither inflation nor purchasing power (see Table 2). If one controls for inflation by using constant prices pegged to a particular baseline, GDP per capita grew by about 3 percent between 2013 and 2019, according to the World Bank data.

Table 2: World Bank Estimates for 2013-2019

Source: World Bank

Footnotes:

- The IMF has updated its data since the FT article came out: The latest World Economic Outlook database is from April 2021; however, we have linked above to the October 2020 database because it is the one that would have been available at the time the FT article was written and published.

- At the time the FT article was published, none of these sources had publicly available data on Russia’s per capita GDP for 2021 and only one had even estimated data for the entirety of the 2013-2020 period: the IMF.

- Even though the numbers currently available from the World Bank differ somewhat from those on offer at the time of the FT publication, that difference is very small (less than 1%).